题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

[主观题]

Make a note of it ______ you should forget it.A.soB.toC.howD.lest

Make a note of it ______ you should forget it.

A.so

B.to

C.how

D.lest

查看答案

如果结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

如果结果不匹配,请 联系老师 获取答案

题目内容

(请给出正确答案)

Make a note of it ______ you should forget it.

A.so

B.to

C.how

D.lest

如果结果不匹配,请 联系老师 获取答案

更多“Make a note of it ______ you s…”相关的问题

更多“Make a note of it ______ you s…”相关的问题

Please fill the following blank form as per the above instructions to make a promissory note.

Promissory Note for ____________ ______, ____________

At __________________ we promise to pay to ____________

______________________________ the sum of ____________

__________________

For __________________

__________________

__________________

Careful note – taking on your reading material ___48___ while you read. Pausing periodically to ___49__ about important claims or ideas, ___50___ details, or questions about unclear concepts. The act of note – taking will help you to reflect about the content of the document, and the notes you keep will ___51___ an archive that you can refer to in the future.

Synthesis is the ability to take what are ___52___ seeming irrelevant points and put them together into a meaningful, new whole. Synthesis may occur during your reading, or it may tale place after you have read a document in its entirety.

Analysis moves synthesis one step ___53___ , encouraging a reader to carefully examine thoroughly the points ___54__ , and how they are synthesized. After readers analyze a passage or a whole text, they ___55__ regarding the document, either generally agreeing or disagreeing with its message. (205 words)

46. A. study B. reflect on C. consider D. think

47. A. and B. but also C. moreover D. yet

48. A. must take place B. may start C. have to begin D. should occur

49. A. make note B. write note C. take notes D. keep note

50. A. relevant B. connected C. associated D. linked

51. A. act as B. serve as C. consider as D. regard as

52. A. firstly B. to begin with C. first hand D. at first

53. A. in advance B. farther C. further D. forwardly

54. A. to be made B. being made C. having made D. to make

55. A. take a position B. insist on C. consider D. hold the view

At first the author looked upon life as a process of getting He formed this view of life because_______.

A.other people were selfish

B.he thought if exciting to get from others

C.of his early education

D.of his character

The author wrote a note of appreciation to the post office because________.A.he knew what such a note would mean to the post office

B.he had discovered giving-away made life all the more exciting

C.he believed he would get something back by doing so.

D.the postman delivered an important letter in time

When the author needed a post-office box,_________.A.he wrote the postmaster a note of appreciation.

B.he asked to put his name on a waiting list.

C.he tried to see the postmaster.

D.many had applied for post-office boxes before him.

The postmaster promised__________.A.to make a new post-office box for the author

B.to let the author have a post-office box.

C.to include the author’s mane on the list.

D.to deliver the author’s mail to his home

The postmaster interfered because_________.A.he was thankful for the letter the author had written

B.he overheard their conversation

C.he was proud of their good service

D.he received a lot of complaints for lack of post-office box

请帮忙给出每个问题的正确答案和分析,谢谢!

It's important for a CEO to be passionate and enthusiastic,but there's a line of professionalism that must

always be maintained.

According to a report from the technology website Venture Beat,PayPal CEO David Marcus wrote a critical letter to his employees blaming them for not using PayPal products and encouraging them to leave if they didn't have the passion to use the products they work for.

According to the website,part of the leaked letter reads:

It's been brought to my attention that when testing paying with mobile at Cafe 17 last week,some of you refused to install the PayPal app,and others didn't even remember their PayPal passwords.That's unacceptable to me,and the rest of my team,everyone at PayPal should use our products where available.That's the only way we can make them better,and better.

In closing,if you are one of the folks who refused to install the PayPal app or if you can't remember your PayPal password,do yourself a favor,go and find something that will connect with your heart and mind elsewhere.

While not obvious at first,the letter reveals a problem of morale and culture at PayPal.As an executive,you certainly want your employees to use and promote your products.However,when faced with a situation where staff isn't embracing what they make,you need to investigate the root of the problem-not threaten.

When faced with internal problems,good executives start by asking why.They reach out to their executive team first and then to the entire staff to find the root of a problem and how to fix it.Sending out a one-sided note about the problem is not leading,it's retreating.

Leadership starts by listening.Good executives need to get out among the staff and ask questions and listen without judgment or reaction.The fact that company employees are not embracing and using its products is a failure of leadership that Marcus needs to address by self-reflection.At the end of the day,if his employees have to be forced to use the app,how can he expect consumers to want to willingly pay to use it? Marcus should have focused on three questions:

Why are you not using the app?

What is it that we can do to ensure you use our app?

What do you need from me?

1.A CEO only needs to be passionate and enthusiastic.

2.It is not professional that PayPal CEO blames his employees not to use PayPal or forget PayPal passwords.

3.A one-sided note refers to the root of PayPal's problem.

4.When faced with internal problems,good executives find the root of a problem in their executive team first.

5.Good executives need to give feedback immediately when they are listening to the staff.

The Right Way to Motivate Employees

It’s important for a CEO to be passionate and enthusiastic, but there’s a line of professionalism that must always be maintained.

According to a report from the technology website Venture Beat, PayPal CEO David Marcus wrote a critical letter to his employees blaming them for not using PayPal products and encouraging them to leave if they didn’t have the passion to use the products they work for.

According to the website, part of the leaked letter reads:

“It’s been brought to my attention that when testing paying with mobile at Cafe 17 last week, some of you refused to install the PayPal app, and others didn’t even remember their PayPal passwords.That’s unacceptable to me, and the rest of my team, everyone at PayPal should use our products where available.That’s the only way we can make them better, and better.”

“In closing, if you are one of the folks who refused to install the PayPal app or if you can’t remember your PayPal password, do yourself a favor, go and find something that will connect with your heart and mind elsewhere.”

While not obvious at first, the letter reveals a problem of morale and culture at PayPal.As an executive, you certainly want your employees to use and promote your products.However, when faced with a situation where staff isn’t embracing what they make, you need to investigate the root of the problem -- not threaten.

When faced with internal problems, good executives start by asking “why”.They reach out to their executive team first and then to the entire staff to find the root of a problem and how to fix it.Sending out a one-sided note about the problem is not leading, it’s retreating.

Leadership starts by listening.Good executives need to get out among the staff and ask questions and listen without judgment or reaction.The fact that company employees are not embracing and using its products is a failure of leadership that Marcus needs to address by self-reflection.At the end of the day, if his employees have to be forced to use the app, how can he expect consumers to want to willingly pay to use it? Marcus should have focused on three questions:

• Why are you not using the app?

• What is it that we can do to ensure you use our app?

• What do you need from me?

1.A CEO only needs to be passionate and enthusiastic.()

2.It is not professional that PayPal CEO blames his employees not to use PayPal or forget PayPal passwords.()

3.“A one-sided note” refers to the root of PayPal’s problem.()

4.When faced with internal problems, good executives find the root of a problem in their executive team first.()

5.Good executives need to give feedback immediately when they are listening to the staff.()

Most of the money today is made of metal or paper. But people used to use all kinds of things as money. One of the first kinds of money was shells.

Shells were not the only things used as money. In China, cloth and 'knives were used. In the Philippine Islands, rice was used as money. In some parts of Africa, cattle were one of the earliest kinds of money. Other animals were used as money, too.

The first metal coins were made in China. They were round and had a square hole in the center. People strung them together and carried them from place to place.

Different countries have used different metals and designs for their money. The first coins in England were made of tin. Sweden and Russia used copper to make their money. Later, other countries began to make coins of gold and silver.

But even gold and silver were inconvenient if you had to buy something expensive. Again the Chinese thought of a way to improve money. They began to use paper money. (80)The first paper money looked more like a note from one person to another than paper money used today.

Money has had an interesting history from the days of shell money until today.

Which of the following can be cited as an example of the use of money in exchange for services?

A.To sell a bicycle for $ 20.

B.To get some money for old books at a garage sale.

C.To buy things you need or want.

D.To get paid for your work.

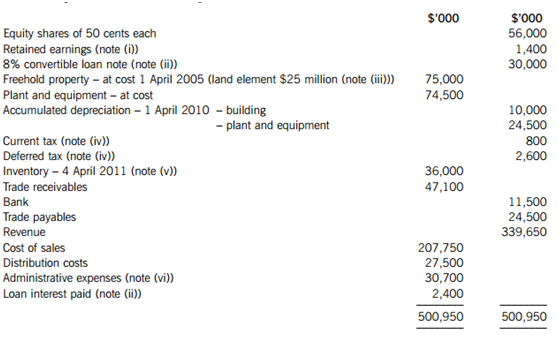

The following trial balance relates to Highwood at 31 March 2011:

The following notes are relevant:

(i) An equity dividend of 5 cents per share was paid in November 2010 and charged to retained earnings.

(ii) The 8% $30 million convertible loan note was issued on 1 April 2010 at par. Interest is payable annually in arrears on 31 March each year. The loan note is redeemable at par on 31 March 2013 or convertible into equity shares at the option of the loan note holders on the basis of 30 equity shares for each $100 of loan note. Highwood’s finance director has calculated that to issue an equivalent loan note without the conversion rights it would have to pay an interest rate of 10% per annum to attract investors.

The present value of $1 receivable at the end of each year, based on discount rates of 8% and 10% are:

(iii) Non-current assets:

On 1 April 2010 Highwood decided for the first time to value its freehold property at its current value. A qualified property valuer reported that the market value of the freehold property on this date was $80 million, of which $30 million related to the land. At this date the remaining estimated life of the property was 20 years. Highwood does not make a transfer to retained earnings in respect of excess depreciation on the revaluation of its assets.

Plant is depreciated at 20% per annum on the reducing balance method.

All depreciation of non-current assets is charged to cost of sales.

(iv) The balance on current tax represents the under/over provision of the tax liability for the year ended 31 March 2010. The required provision for income tax for the year ended 31 March 2011 is $19·4 million. The difference between the carrying amounts of the net assets of Highwood (including the revaluation of the property in note (iii) above) and their (lower) tax base at 31 March 2011 is $27 million. Highwood’s rate of income tax is 25%.

(v) The inventory of Highwood was not counted until 4 April 2011 due to operational reasons. At this date its value at cost was $36 million and this figure has been used in the cost of sales calculation above. Between the year end of 31 March 2011 and 4 April 2011, Highwood received a delivery of goods at a cost of $2·7 million and made sales of $7·8 million at a mark-up on cost of 30%. Neither the goods delivered nor the sales made in this period were included in Highwood’s purchases (as part of cost of sales) or revenue in the above trial balance.

(vi) On 31 March 2011 Highwood factored (sold) trade receivables with a book value of $10 million to Easyfinance. Highwood received an immediate payment of $8·7 million and will pay Easyfinance 2% per month on any uncollected balances. Any of the factored receivables outstanding after six months will be refunded to Easyfinance. Highwood has derecognised the receivables and charged $1·3 million to administrative expenses. If Highwood had not factored these receivables it would have made an allowance of $600,000 against them.

Required:

(i) Prepare the statement of comprehensive income for Highwood for the year ended 31 March 2011;

(ii) Prepare the statement of changes in equity for Highwood for the year ended 31 March 2011;

(iii) Prepare the statement of financial position of Highwood as at 31 March 2011.

Note: your answers and workings should be presented to the nearest $1,000; notes to the financial statements are not required.

The following mark allocation is provided as guidance for this question:

(i) 11 marks

(ii) 4 marks

(iii) 10 marks

From the passage, we understand that______.

A.the author did not understand the importance of giving until he was in late thirties

B.the author was like most people who were mostly receivers rather than givers

C.the author received the same education as most people during his childhood

D.the author liked most people as they looked upon life as a process of getting

(a) A director of Enca, a public listed company, has expressed concerns about the accounting treatment of some of the company’s items of property, plant and equipment which have increased in value. His main concern is that the statement of financial position does not show the true value of assets which have increased in value and that this ‘undervaluation’ is compounded by having to charge depreciation on these assets, which also reduces reported profit. He argues that this does not make economic sense.

Required:

Respond to the director’s concerns by summarising the principal requirements of IAS 16 Property, Plant and Equipment in relation to the revaluation of property, plant and equipment, including its subsequent treatment.

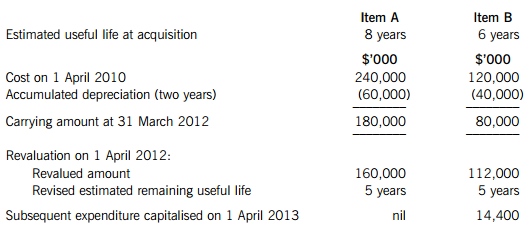

(b) The following details relate to two items of property, plant and equipment (A and B) owned by Delta which are depreciated on a straight-line basis with no estimated residual value:

At 31 March 2014 item A was still in use, but item B was sold (on that date) for $70 million.

Note: Delta makes an annual transfer from its revaluation surplus to retained earnings in respect of excess depreciation.

Required:

Prepare extracts from:

(i) Delta’s statements of profit or loss for the years ended 31 March 2013 and 2014 in respect of charges (expenses) related to property, plant and equipment;

(ii) Delta’s statements of financial position as at 31 March 2013 and 2014 for the carrying amount of property, plant and equipment and the revaluation surplus.

The following mark allocation is provided as guidance for this requirement:

(i) 5 marks

(ii) 5 marks (10 marks)

The count will be undertaken by 15 teams of two counters from the warehouse department with Quartz’s financial controller providing overall supervision. Each team of two is allocated a number of bays within the warehouse to count and they are provided with sequentially numbered inventory sheets which contain product codes and quantities extracted from the inventory records. The counters move through each allocated bay counting the inventory and confirming that it agrees with the inventory sheets. Where a discrepancy is found, they note this on the sheet.

The warehouse is large and approximately 10% of the bays have been rented out to third parties with similar operations; these are scattered throughout the warehouse. For completeness, the counters have been asked to count the inventory for all bays noting the third party inventories on separate blank inventory sheets, and the finance department will make any necessary adjustments.

Some of Quartz’s finished goods are high in value and are stored in a locked area of the warehouse and all the counting teams will be given the code to access this area. There will be no despatches of inventory during the count and it is not anticipated that there will be any deliveries from suppliers.

Each area is counted once by the allocated team; the sheets are completed in ink, signed by the team and returned after each bay is counted. As no two teams are allocated the same bays, there will be no need to flag that an area has been counted. On completion of the count, the financial controller will confirm with each team that they have returned their inventory sheets.

Required:

(a) In respect of the inventory count procedures for Lemon Quartz Co:

(i) Identify and explain FIVE deficiencies;

(ii) Recommend a control to address each of these deficiencies; and

(iii) Describe a TEST OF CONTROL the external auditors would perform. to assess if each of these controls, if implemented, is operating effectively.

Note: The total marks will be split equally between each part. (15 marks)

(b) Quartz’s finance director has asked your firm to undertake a non-audit assurance engagement later in the year. The audit junior has not been involved in such an assignment before and has asked you to explain what an assurance engagement involves.

Required:

Explain the five elements of an assurance engagement. (5 marks)