Section A – This ONE question is compulsory and MUST be attemptedCocoa-Mocha-Chai (CMC) Co

Section A – This ONE question is compulsory and MUST be attempted

Cocoa-Mocha-Chai (CMC) Co is a large listed company based in Switzerland and uses Swiss Francs as its currency. It imports tea, coffee and cocoa from countries around the world, and sells its blended products to supermarkets and large retailers worldwide. The company has production facilities located in two European ports where raw materials are brought for processing, and from where finished products are shipped out. All raw material purchases are paid for in US dollars (US$), while all sales are invoiced in Swiss Francs (CHF).

Until recently CMC Co had no intention of hedging its foreign currency exposures, interest rate exposures or commodity price fluctuations, and stated this intent in its annual report. However, after consultations with senior and middle managers, the company’s new Board of Directors (BoD) has been reviewing its risk management and operations strategies.

The following two proposals have been put forward by the BoD for further consideration:

Proposal one

Setting up a treasury function to manage the foreign currency and interest rate exposures (but not commodity price fluctuations) using derivative products. The treasury function would be headed by the finance director. The purchasing director, who initiated the idea of having a treasury function, was of the opinion that this would enable her management team to make better decisions. The finance director also supported the idea as he felt this would increase his influence on the BoD and strengthen his case for an increase in his remuneration.

In order to assist in the further consideration of this proposal, the BoD wants you to use the following upcoming foreign currency and interest rate exposures to demonstrate how they would be managed by the treasury function:

(i) a payment of US$5,060,000 which is due in four months’ time; and

(ii) a four-year CHF60,000,000 loan taken out to part-fund the setting up of four branches (see proposal two below). Interest will be payable on the loan at a fixed annual rate of 2·2% or a floating annual rate based on the yield curve rate plus 0·40%. The loan’s principal amount will be repayable in full at the end of the fourth year.

Proposal two

This proposal suggested setting up four new branches in four different countries. Each branch would have its own production facilities and sales teams. As a consequence of this, one of the two European-based production facilities will be closed. Initial cost-benefit analysis indicated that this would reduce costs related to production, distribution and logistics, as these branches would be closer to the sources of raw materials and also to the customers. The operations and sales directors supported the proposal, as in addition to above, this would enable sales and marketing teams in the branches to respond to any changes in nearby markets more quickly. The branches would be controlled and staffed by the local population in those countries. However, some members of the BoD expressed concern that such a move would create agency issues between CMC Co’s central management and the management controlling the branches. They suggested mitigation strategies would need to be established to minimise these issues.

Response from the non-executive directors

When the proposals were put to the non-executive directors, they indicated that they were broadly supportive of the second proposal if the financial benefits outweigh the costs of setting up and running the four branches. However, they felt that they could not support the first proposal, as this would reduce shareholder value because the costs related to undertaking the proposal are likely to outweigh the benefits.

Additional information relating to proposal one

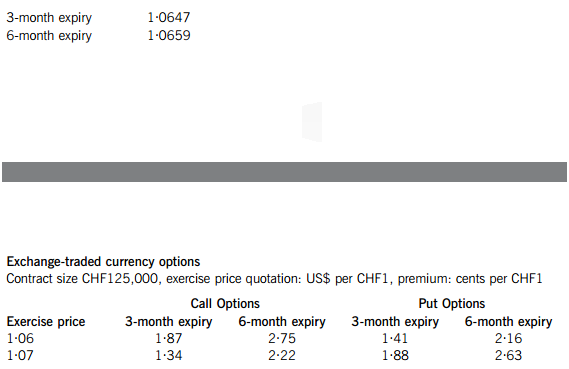

The current spot rate is US$1·0635 per CHF1. The current annual inflation rate in the USA is three times higher than Switzerland.

The following derivative products are available to CMC Co to manage the exposures of the US$ payment and the interest on the loan:

Exchange-traded currency futures

Contract size CHF125,000 price quotation: US$ per CHF1

It can be assumed that futures and option contracts expire at the end of the month and transaction costs related to these can be ignored.

Over-the-counter products

In addition to the exchange-traded products, Pecunia Bank is willing to offer the following over-the-counter derivative products to CMC Co:

(i) A forward rate between the US$ and the CHF of US$ 1·0677 per CHF1.

(ii) An interest rate swap contract with a counterparty, where the counterparty can borrow at an annual floating rate based on the yield curve rate plus 0·8% or an annual fixed rate of 3·8%. Pecunia Bank would charge a fee of 20 basis points each to act as the intermediary of the swap. Both parties will benefit equally from the swap contract.

Required:

(a) Advise CMC Co on an appropriate hedging strategy to manage the foreign exchange exposure of the US$ payment in four months’ time. Show all relevant calculations, including the number of contracts bought or sold in the exchange-traded derivative markets. (15 marks)

(b) Demonstrate how CMC Co could benefit from the swap offered by Pecunia Bank. (6 marks)

(c) As an alternative to paying the principal on the loan as one lump sum at the end of the fourth year, CMC Co could pay off the loan in equal annual amounts over the four years similar to an annuity. In this case, an annual interest rate of 2% would be payable, which is the same as the loan’s gross redemption yield (yield to maturity).

Required: Calculate the modified duration of the loan if it is repaid in equal amounts and explain how duration can be used to measure the sensitivity of the loan to changes in interest rates. (7 marks)

(d) Prepare a memorandum for the Board of Directors (BoD) of CMC Co which:

(i) Discusses proposal one in light of the concerns raised by the non-executive directors; and (9 marks)

(ii) Discusses the agency issues related to proposal two and how these can be mitigated. (9 marks)

Professional marks will be awarded in part (d) for the presentation, structure, logical flow and clarity of the memorandum. (4 marks)

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

如果结果不匹配,请 联系老师 获取答案

如果结果不匹配,请 联系老师 获取答案

更多“Crag Co has sales of $200m per…”相关的问题

更多“Crag Co has sales of $200m per…”相关的问题